Despite signs of improving financial conditions and renewed government focus on housing reform, New Zealand’s construction sector remains cautious.

The latest 2025 National Specifier Survey, conducted in late 2025 by the CMS Group (CMS), reveals an industry that is not short of work or ambition, but is mixed in converting intent into action. Across more than 1,000 responses, a consistent picture emerges: projects are being discussed, designed and planned, yet some are failing to progress beyond the gate.

At the heart of hesitation lies a combination of regulatory uncertainty, council consenting and inspection delays, rising costs, and fragile confidence, all set against the backdrop of recent business failures across the sector.

We pulled together some key comments and themes from across the survey to get a snapshot of what matters and what might be holding us back.

A sector under strain, but not short of ideas

Over the past six months, the construction industry has seen a steady flow of liquidations and insolvencies, particularly among small and mid-sized builders, subcontractors and specialist trades.

Rising input costs, delayed payments, prolonged consenting processes and tightening margins have reportedly combined to push many firms beyond their limits.

Although industry observers note that an Inland Revenue Department compliance crackdown has accelerated the closure of marginal businesses, with outstanding tax liabilities and historical debt called in at a time when cash flow is already under pressure.

The cumulative effect has reduced industry capacity and heightened caution across the sector.

Excerpt from The CMS Group 2025 National Specifier Survey report

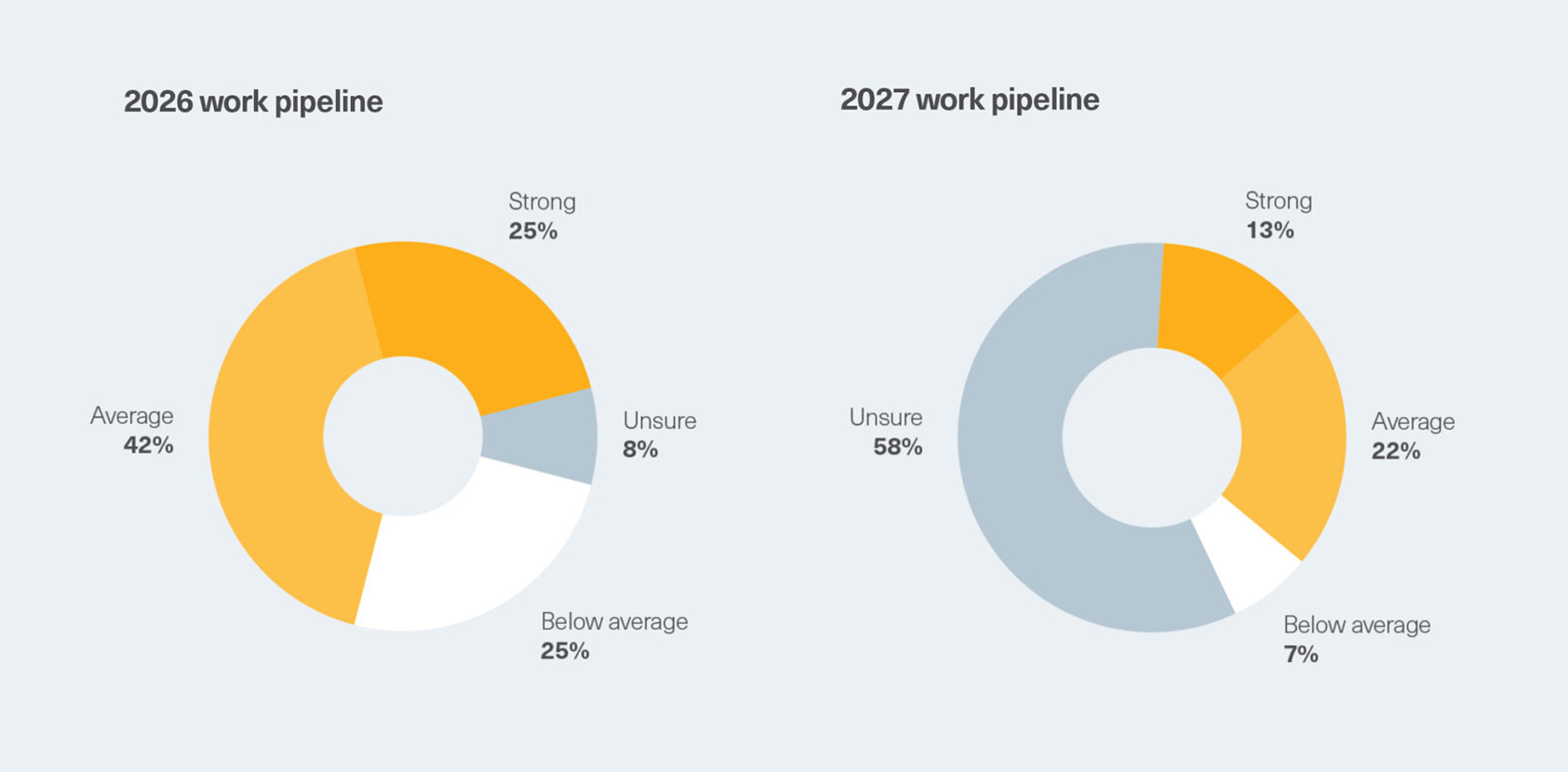

The CMS survey suggests the construction pipeline, however, has not collapsed. For 2026, most respondents described their workload as average or strong, indicating that demand and interest remain.

However, confidence is more uncertain when looking further ahead. Nearly 60 percent of respondents said they were unsure about their 2027 pipeline, and only 13 percent described it as strong. Fewer than half were confident that projects currently on hold would proceed.

As one respondent put it:

“Just the ability to pull the trigger on some jobs due to the current instability of finances across the country… Goal posts keep moving.”

This suggests that projects and buyer interest exist. What’s missing is certainty.

Council red tape: a perennial issue

Across hundreds of open-text responses, council consenting and compliance processes emerged as one of the most consistent and deeply felt frustrations.

Respondents described a system that is slow, unpredictable and increasingly expensive to navigate — even for relatively modest projects.

“Build costs are high, added to by the myriad of consenting costs and requirements. A simple resource consent seems to require tens of thousands of dollars’ worth of consultants alone.”

Others pointed to inconsistency as the core issue.

“Consenting and compliance costs — and the lack of consistency. Every council appears to interpret things differently.”

While the government has signalled reforms aimed at speeding up housing consents, the survey suggests policy intent has yet to translate into confidence on the ground. In many cases, respondents said uncertainty has increased during periods of transition, as councils adjust to new direction.

“Blue tape through councils stalling consents over minor issues and inexperienced staff.”

Inspections: the hidden tripwire

Inspection processes were repeatedly cited as a growing source of cost escalation and delay.

Respondents described inconsistent interpretations of the Building Code, variable health and safety requirements, and inspection delays that disrupt construction sequencing and programme certainty.

“Increasing costs of compliance. Health and safety is not consistent, and every client appears to have their own spin on it.”

For builders and clients alike, this inconsistency introduces risk. Trades wait on site. Programmes stretch. Budgets inflate without adding value.

In response, risk tolerance drops, innovation is discouraged, and conservative design becomes the safest option.

Legislative change and intensification uncertainty

Beyond cost and process, regulatory uncertainty itself has become a major brake on confidence.

Recent changes and proposed adjustments to housing and intensification rules, particularly in Auckland, have created ambiguity around what can be built, where density will be supported, and how councils are expected to apply national direction.

While intensification is widely accepted as necessary, respondents repeatedly noted that transitional uncertainty has delayed decisions, particularly for medium-density and infill housing.

“Confusion around the new 70m² non-consented dwellings. Unnecessarily high costs associated with small projects.”

Others linked legislative change directly to hesitation.

“Uncertainty — internationally and domestically, but especially at council level.”

The issue is not opposition to reform, but the gap between policy announcements and delivery reality. Until rules stabilise and interpretation aligns, many projects remain on hold.

House prices not meeting expectations

Compounding regulatory uncertainty is a slower-than-expected recovery in house prices.

Many residential developments were modelled on assumptions of modest price growth to offset rising construction and compliance costs. Instead, prices in many markets have remained flat, while costs have continued to climb.

“Getting projects to meet budgets and end sale values.”

Another respondent noted:

“Cost of building in general is high compared to existing housing stock.”

While prices have begun to rise and are predicted to average +1.9% house price growth to the year ending June 2026 (New Zealand Treasury forecasts) and ~5% annually from 2027 onward, that rate of increase is not yet enough to soak up existing stock and drive real growth in the short term.

Finance: improving signals, fragile confidence

At a macro level, financial conditions appear to be easing. Reserve Bank data shows M3 money supply reached a record $447.9 billion in December 2025, reflecting increased lending capacity, including for new mortgages.

Historically, such conditions would support a lift in construction activity.

Yet survey respondents suggest this capacity has not translated into confidence — particularly in a sector still absorbing the impact of recent insolvencies.

“Finance, cashflow — customers want more for less, but costs keep rising.”

Others pointed to the timing mismatch between finance and approvals.

“Lending and committing to a renovation are harder when approvals take so long.”

In practice, respondents described finance as conditional and time-sensitive, with approvals expiring while projects wait in the consent system.

Cost inflation hasn’t gone away

Concern about product and building material price inflation remains deeply embedded across survey responses.

While headline inflation has eased from its peak, construction inputs have not followed the same path. Material costs, compliance costs and labour rates continue to rise, eroding feasibility even as demand stabilises.

“Material cost increases, compliance cost increases, labour increases — generally the cost of building is going up.”

Supply delays further compound the problem.

“If something cost X in June, by the time it’s available months later, the cost could well have gone up again.”

These pressures collide with renewed concern from the Reserve Bank that inflation may remain higher than expected, particularly in non-tradable sectors such as construction, raising the prospect that mortgage rates may stay higher for longer, or rise again.

For home buyers and small developers, even the expectation of higher rates is enough to delay decisions.

“Affordability with increasing costs.”

A narrowing window for confidence

Taken together, the survey responses suggest the sector is operating with very limited tolerance for additional shocks.

Legislative change, planning uncertainty, flat house prices, material inflation and interest rate sensitivity form a feedback loop. Each delay increases exposure to the next risk.

“Cost overrun and delay.”

In this sense, inefficiency in consenting and inspection processes is not merely frustrating; it is inflationary, amplifying risk the longer projects remain stalled.

It’s not a call for deregulation — it’s a call for certainty

Importantly, the CMS survey does not reveal an industry calling for fewer rules. Instead, it points to a desire for clarity, consistency and predictability.

Respondents want to know:

- What is required

- How long will it take

- What it will cost

…before committing capital, labour and time.

“Budget versus expectation and need.”

“Having the confidence in the market to proceed with projects.”

Until those conditions improve, not just in policy, but in practice, improved financial settings alone may not be enough to unlock momentum.

The risk of standing still

The greatest risk facing the construction sector may not be a lack of demand, but the normalisation of delay and uncertainty.

When projects stall at the gate, capacity erodes quietly. Skills are underutilised. Supply chains lose momentum. Investment hesitates.

The CMS National Survey of Specifiers suggests New Zealand still has the expertise, demand and capital to build. What it increasingly lacks is a system that reliably converts those inputs into action.

Unless consenting and inspection processes become clearer, faster and more consistent, even positive economic signals may continue to fall short of their intended impact.

As one respondent put it simply:

“Having the means, and the confidence, to do the work.”

This article draws on findings from the CMS National Survey of Specifiers — architects, designers, engineers and builders — alongside anonymised qualitative responses, recent housing policy reporting and Reserve Bank of New Zealand data.